")

Markets are entering mid-October with sharp contrasts across asset classes. Silver continues to dominate headlines after touching record highs near $49.5 per ounce, extending a remarkable 60% year-to-date rally fueled by safe-haven demand and a weaker U.S. dollar. In equities, Jefferies is under scrutiny after a strong third quarter was overshadowed by credit exposure to the First Brands bankruptcy, raising questions about balance-sheet risk despite solid advisory momentum. Meanwhile, in currencies, GBP/JPY has surged to a 15-month high around 204.4, as Japan's political shift toward fiscal stimulus deepens yen weakness while the pound remains supported by resilient UK data and cautious BoE policy. Together, these moves highlight a market landscape driven by divergent policy paths, tightening liquidity, and growing sensitivity to macro catalysts.

Silver Soars, Jefferies Stumbles and Yen Slides

Markets are entering mid-October with sharp contrasts across asset classes. Silver continues to dominate headlines after touching record highs near $49.5 per ounce, extending a remarkable 60% year-to-date rally fueled by safe-haven demand and a weaker U.S. dollar. In equities, Jefferies is under scrutiny after a strong third quarter was overshadowed by credit exposure to the First Brands bankruptcy, raising questions about balance-sheet risk despite solid advisory momentum. Meanwhile, in currencies, GBP/JPY has surged to a 15-month high around 204.4, as Japan's political shift toward fiscal stimulus deepens yen weakness while the pound remains supported by resilient UK data and cautious BoE policy. Together, these moves highlight a market landscape driven by divergent policy paths, tightening liquidity, and growing sensitivity to macro catalysts.

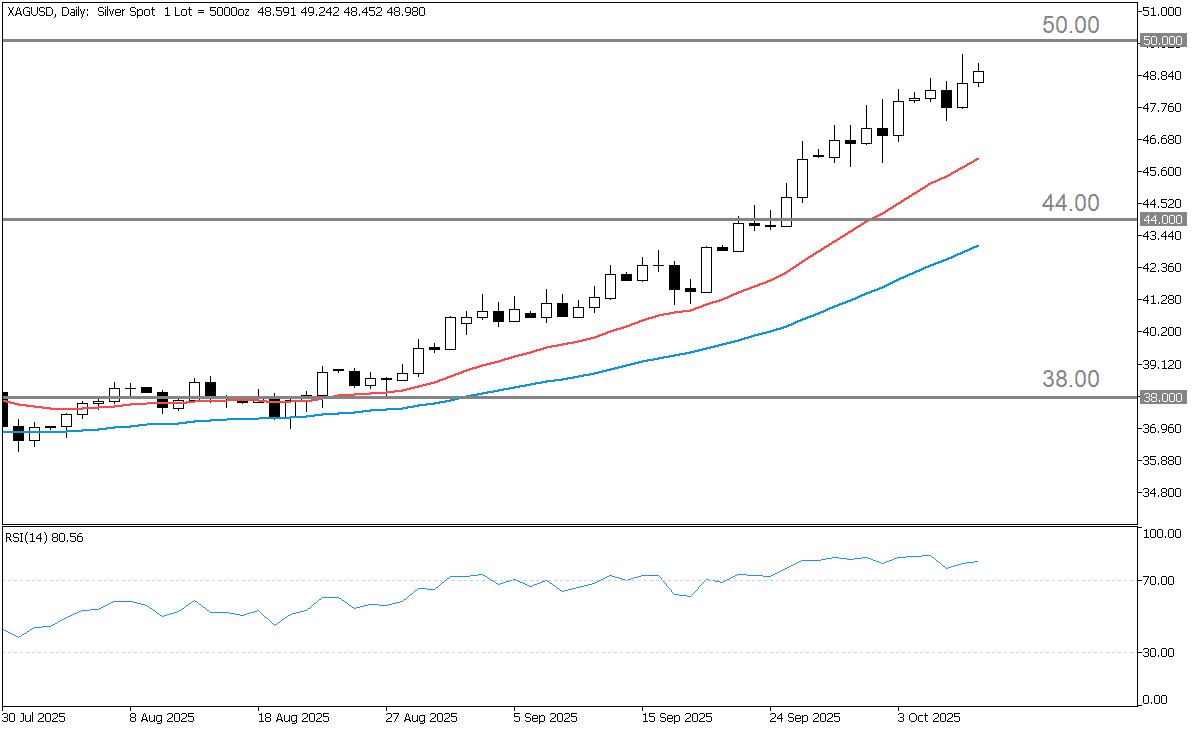

Silver Hits Record Highs as Rally Matures and Volatility Looms

Silver has been in a powerful uptrend throughout 2025, with year-to-date gains exceeding 60%. On October 8, 2025, the metal reached an all-time high near $49.525 per ounce. The surge has been closely linked to gold's record-breaking rally above $4,000 per ounce, driven by safe-haven inflows and a weakening U.S. dollar, which have broadly lifted precious metals. However, while fundamentals and sentiment remain supportive, analysts caution that extreme overbought technical conditions and exceptionally tight inventory and lease rates could signal a potential cooling ahead. Silver is trading near $48/oz as of the time of writing, suggesting the market is now in a more mature phase of its rally, with heightened sensitivity to catalysts such as monetary policy shifts, USD fluctuations, and supply imbalances.

Silver's Rally Shines, but Overheating Risks Loom

Silver's 2025 rally is being fueled by dovish Federal Reserve expectations, a weaker U.S. dollar, and ongoing supply tightness. As a non-yielding asset, it benefits from lower real interest rates, and markets are still anticipating additional Fed cuts before year-end. A soft dollar continues to support precious metals, though any sharp rebound in yields could weigh on prices. On the supply side, record-high lease rates highlight scarce inventories, but normalization in Chinese and Indian flows could ease the squeeze. Industrial demand from solar and electronics provides long-term support, though elevated prices may start to curb usage. While momentum and sentiment remain strong, overbought technical indicators and stretched positioning suggest the rally may soon enter a period of consolidation or correction.

Silver's Path Ahead: Breakout, Breather, or Breakdown?

Silver's near-term outlook can be viewed through three possible scenarios. In a bullish continuation, if the Federal Reserve proceeds with rate cuts, the U.S. dollar weakens, and inventories remain tight, prices could extend beyond $50, potentially testing the $52–55 zone. This scenario aligns with current sentiment but depends on sustained macro support. In a base or consolidation phase, mixed rate signals, mild profit-taking, or a brief dollar rebound could keep silver trading between $44 and $48, forming a higher base before the next leg up—a healthy pause within an ongoing uptrend. In the bearish case, a hawkish policy surprise, stronger yields or dollar, and easing supply constraints could trigger a correction toward $38–42, testing lower channel support. While this downside scenario is less likely, it becomes more relevant as technical indicators remain overbought and the market grows prone to sharp reversals.

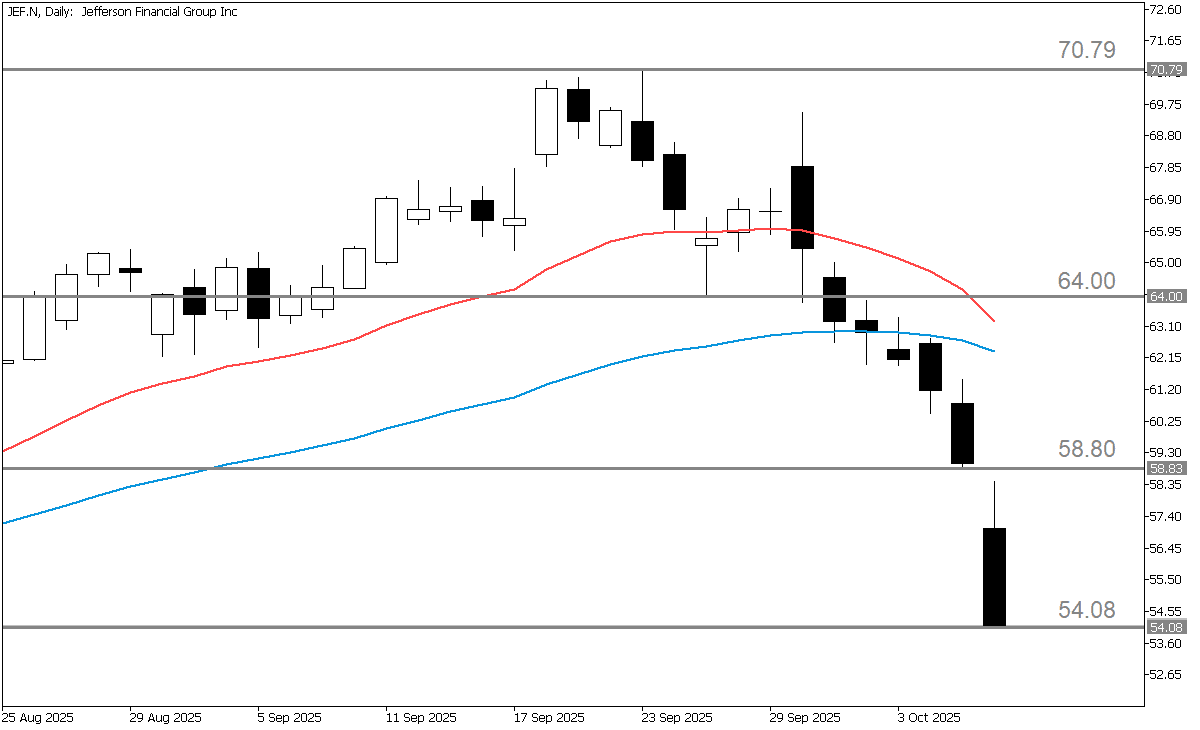

Jefferies Stumbles on First Brands Fallout After Strong Q3

Jefferies sold off after disclosing sizable trade-finance exposure tied to the bankruptcy of First Brands, even as core investment-banking trends remain constructive post–Q3 results. Shares are trading near the mid-50s after an intraday low around $54.08.

Advisory Boom Puts Jefferies Back in the Spotlight

Jefferies operates a diversified investment bank and capital-markets platform with advisory, underwriting, and sales & trading, alongside alternative-asset/credit strategies housed under Leucadia Asset Management. Recent momentum has been most visible in advisory revenues, reflecting a tentative M&A rebound.

Jefferies Beats Forecasts as M&A Momentum Lifts Earnings

During the third quarter of FY2025, Jefferies delivered a strong performance, with investment-banking net revenues rising about 20% year-over-year, marking a record quarter for advisory activity. The company benefited from a revival in dealmaking as interest rates began to ease and corporate confidence improved, helping Jefferies beat market expectations. Management noted that pipelines in mergers, acquisitions, and capital markets underwriting have strengthened, reflecting a more favorable macroeconomic backdrop. In terms of shareholder returns, the board declared a quarterly dividend of $0.40 per share, payable on November 26, 2025, to shareholders of record as of November 17.

Jefferies Eyes Growth but Credit Clouds Keep Investors Guarded

In the primary scenario, Jefferies is expected to sustain moderate deal activity over the next few quarters, with selective improvement in underwriting as market sentiment steadies. Credit reserves linked to the First Brands bankruptcy appear manageable but could introduce short-term earnings volatility, keeping investor sentiment neutral to cautiously positive. Headline risks remain elevated, limiting near-term upside.

In a bullish scenario, a stronger rebound in mergers and acquisitions and renewed equity issuance could lift investment-banking revenues and profitability. If trade-finance losses remain contained, Jefferies would likely maintain its dividend and benefit from improving market confidence, supporting modest valuation gains as dealmaking accelerates.

Conversely, a bearish outcome would stem from deeper credit or legal issues tied to the First Brands case, leading to margin pressure and lower confidence in the firm's balance sheet. Broader market softness could further weigh on sentiment and earnings.

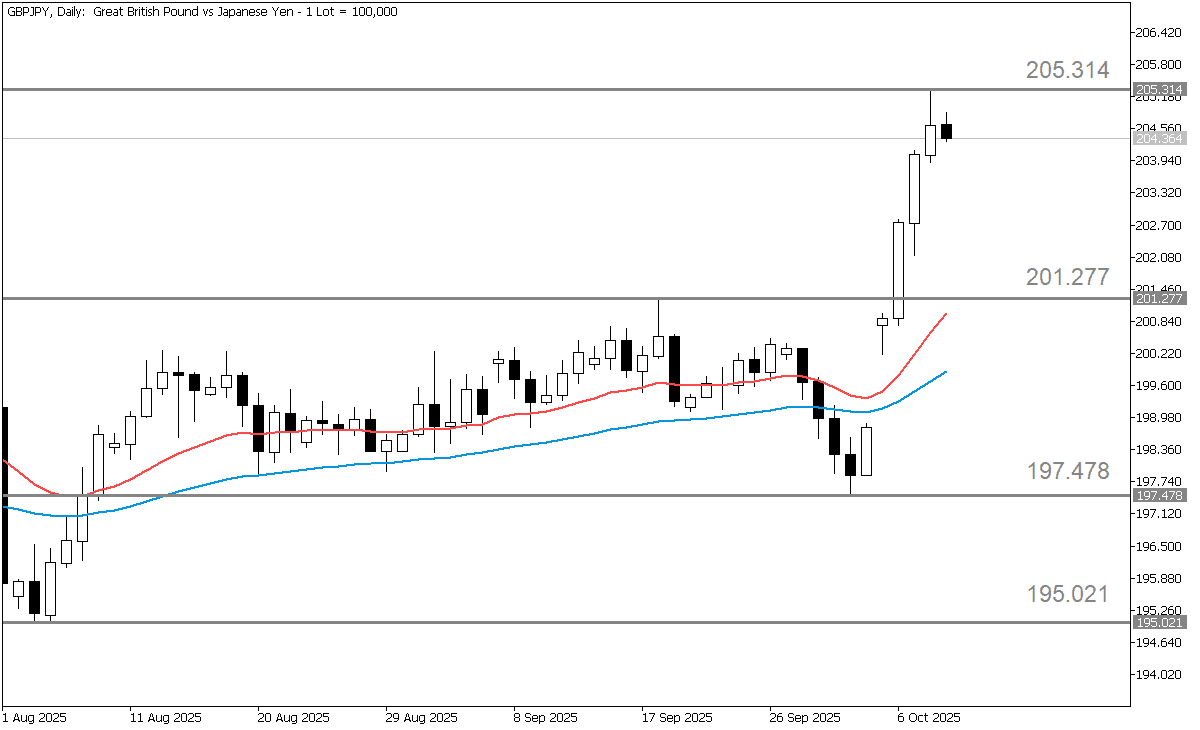

GBP/JPY Hits 15-Month High as Yen Weakens and Pound Holds Its Ground

GBP/JPY is trading near 204.4, marking a 15-month high as the pound sterling continues to strengthen against the yen. The yen has come under sharp pressure in recent sessions, largely due to political and policy developments in Japan that have fueled expectations of looser fiscal conditions and delayed monetary tightening. Over the course of 2025, the pair has fluctuated between roughly 197.50 and 201. With the currency pair now hovering near its yearly highs, momentum appears tilted toward further yen weakness, or at least sustained downside risk for the Japanese currency.

Fresh Wave of Yen Weakness

The election of Sanae Takaichi as LDP leader has fueled expectations of looser fiscal policy, weakening the yen further. Markets have delayed BoJ rate-hike expectations, anticipating continued support for growth. However, rising import costs from a weaker yen may pressure the BoJ to act sooner, with some suggesting a hike by December. Japan's soft growth and higher debt issuance also weigh on the currency. Overall, the outlook remains tilted toward continued yen weakness unless the BoJ intervenes or tightens more aggressively.

Sterling Holds Firm as BoE Walks a Tightrope on Rates

The UK economy remains under pressure, with weaker growth forecasts, persistent inflation, and limited scope for aggressive monetary tightening. The Bank of England faces a balancing act—keeping rates high risks hurting growth, while cutting too soon could reignite inflation. Markets currently see little chance of a rate cut in November, with some expecting policy easing only in 2026. Despite these challenges, sterling has shown relative strength, supported by firmer UK data compared to Japan and investor preference for higher-yielding currencies. However, downside risks persist, including sluggish GDP growth, potential fiscal or political missteps, and shifts toward global risk aversion, which typically benefit the yen.